The World Bank has upgraded its Indian GDP growth forecast from 6.5% to 6.9% for 2022-23. In its latest India Development Update, the UN institution said the revision was due to the higher resilience of the Indian economy to global shocks and better-than-expected second-quarter numbers.

The World Bank had previously been lowering India’s FY23 growth forecast in its World Economic Outlook report thrice consecutively. In October, it had slashed India’s GDP forecast by 1% to 6.5% from its June estimate of 7.5%. It then cited the impact of the ongoing Russia-Ukraine conflict, rising global interest rates and high inflation.

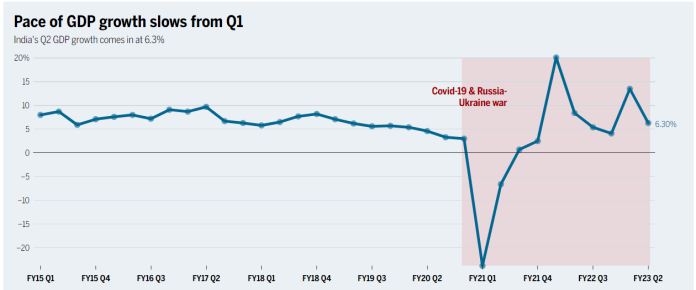

The economy of India grew at 6.3% in the July-September quarter of 2022-23 as compared to 13.5% in the preceding June quarter, mainly on account of contraction in the output of manufacturing and mining sectors.

This is the first upgrade of India’s growth forecast by any international agency amid the global turmoil.

Why did the World Bank revise its forecast for India upward?

Fastest growing economy

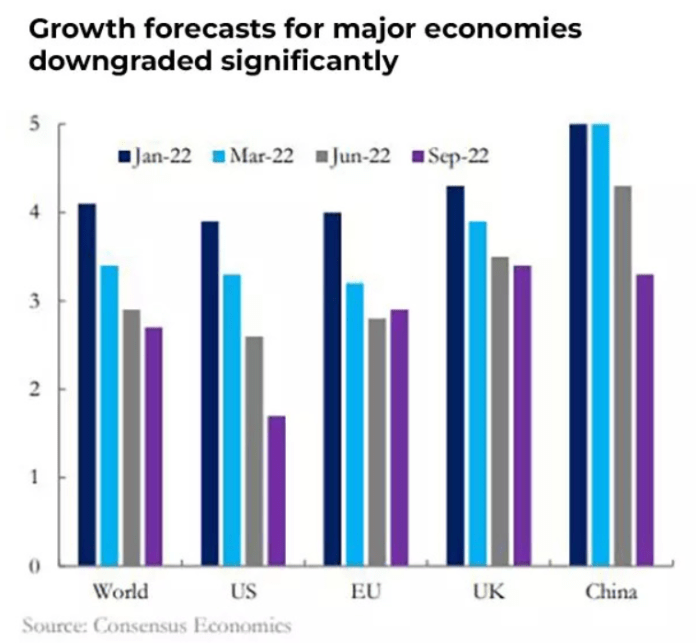

Amid the prevalent global challenges like a tightening monetary policy cycle, slowing growth and elevated commodity prices, the Indian economy will experience lower growth in the 2022-23 financial year compared to 2021-22. However, it reiterated that despite such challenges, India will register strong GDP growth and remain one of the fastest-growing major economies in the world, due to robust domestic demand.

The growth in the first half of FY22-23 was supported by solid domestic demand despite a challenging external environment, the report said. The World Bank noted that exports performed better than expected despite challenging global growth conditions caused by slowing growth in major trade partners (the US, UK and China), the Russia-Ukraine war and persistent global supply disruptions (caused by a global shortage of shipping containers and supply bottlenecks).

In contrast, other emerging market economies (EMEs) — China, Mexico and Brazil — decelerated in July-September 2022 quarter.

More insulated

The report titled “Navigating the Storm” underscored the fact that the Indian economy was relatively more insulated from a global cascading effect than other emerging markets. “India is less exposed to international trade flows and relies on its large domestic market,” it said.

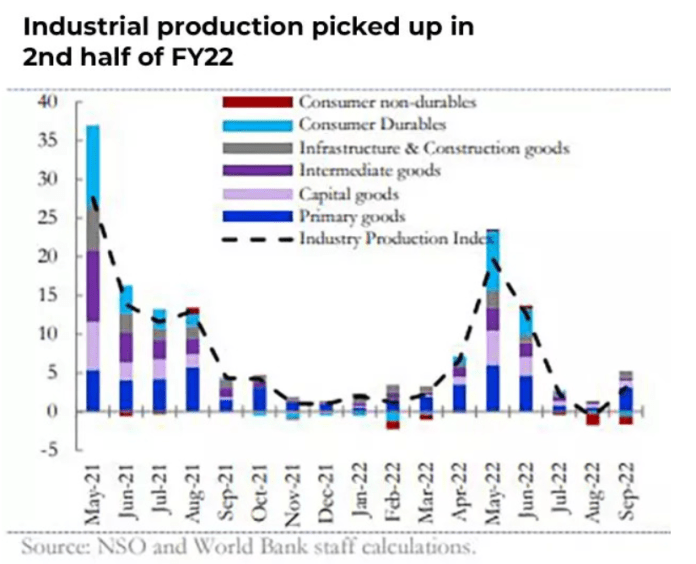

High-frequency indicators show that private consumption and investment continued to grow strongly in October.

Electricity generation and freight traffic remained firmly above pre-pandemic levels. Similarly, passenger vehicle sales and air passenger traffic grew sharply (albeit still below pre-pandemic levels).

Sensex, Nifty at a record high

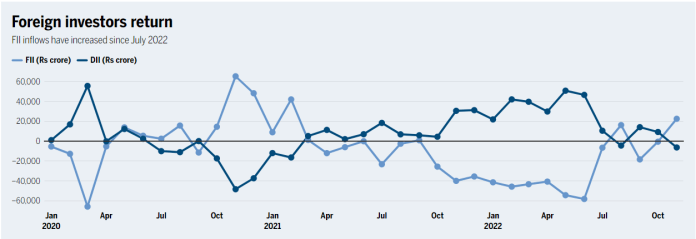

After the decline witnessed in the initial days of the Russia-Ukraine war, Sensex, as well as Nifty, has now bounced back driven by better-than-expected corporate earnings in the first quarter of FY22-23, moderation in domestic inflation and global commodity prices.

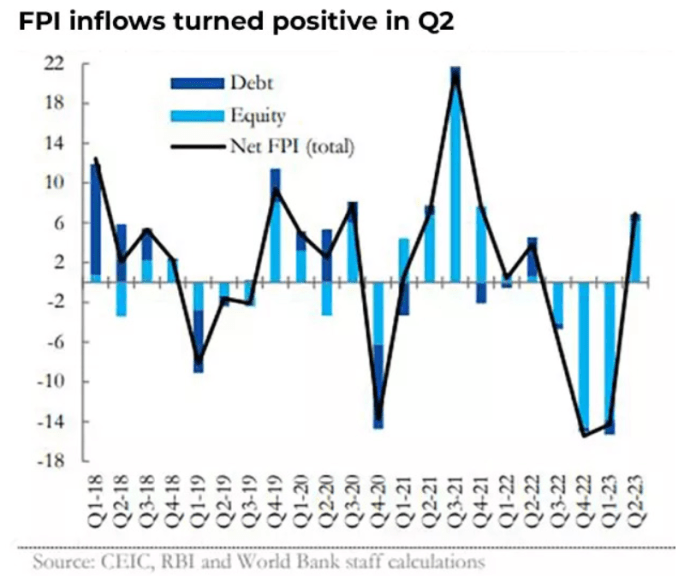

Besides, the return of foreign portfolio investors has also boosted investor sentiments.

Both Sensex and Nifty scaled new highs over the first half of FY22. But experienced a downward trend from October 2022. The rest of the financial year was dampened by policy normalization in advanced economies and geopolitical risks arising from the Ukraine-Russia conflict.

Financial sector growth

The financial sector has deepened considerably over the years but is still recovering from a long period of stress and thus lags relative to other EMEs in terms of capital adequacy and NPL ratios.

Corporate and household debt has declined and remains benign but public debt has increased sharply, as a share of GDP — driven by the pandemic. However, increased market borrowing has improved the transparency and credibility of fiscal policy.

The government has, meanwhile, diversified the investor base for government securities. In addition, inflation targeting by the Reserve Bank of India (RBI) has helped to anchor inflation expectations and price stability has improved.

Boost in private consumption, investment

The report noted that private consumption and investment grew strongly, despite high inflation and borrowing costs. This sharp rise in private consumption was bolstered by festive-season spending in September.

The rise in private consumption has offset a contraction in government consumption caused by fiscal consolidation and the gradual withdrawal of pandemic-related stimulus, the World Bank said.

Likewise, investment growth has remained robust on the back of the union government’s capex push, despite global uncertainty and rising costs amid monetary policy normalisation.

The rise in services output

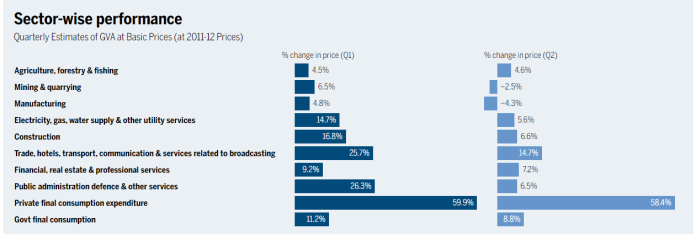

The World Bank report also noted that the services sector expanded 9.3% year-on-year as compared to 10.5% in Q2 of FY23 on the back of solid growth in business services, contact-intensive segments of retail trade, transport, hotels and restaurants, and public administration.

Agriculture sector growth accelerated to 4.6% despite erratic monsoon season and export restrictions on wheat and rice products. However, the manufacturing sector continued to be adversely impacted by slowing external demand, global supply chain disruptions and higher input costs. This resulted in a 4.3% contraction in output.

Rupee better placed

The Indian rupee has fared relatively well in 2022 in comparison to other emerging market peers, senior World Bank economist Dhruv Sharma said. “The rupee has depreciated just about 10% over the course of this year. That might sound like a large number, but relative to many other emerging market peers, India hasn’t fared that badly,” Sharma said after the launch of the India Development Update by the World Bank titled “Navigating the Storm”.

The rupee had plummeted to a record low of 83 against the US dollar in mid-October, triggered by tightening monetary policy by the US Federal Reserve and central banks in other advanced economies. However, it has now come off lows and is currently around 82 against the US dollar.

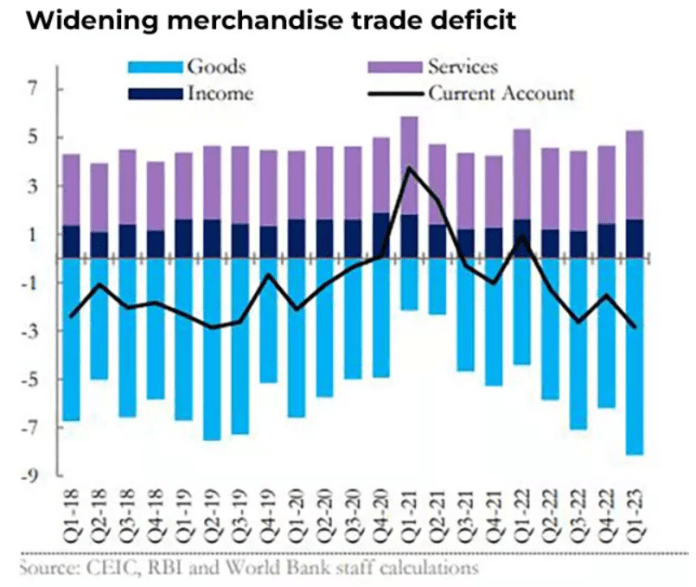

Exports higher than expected

Despite a challenging external environment, exports performed better than expected. However, exports are susceptible to a global growth slowdown - the income elasticity of exports is high, which implies that the global demand for India’s goods and services is cyclical.

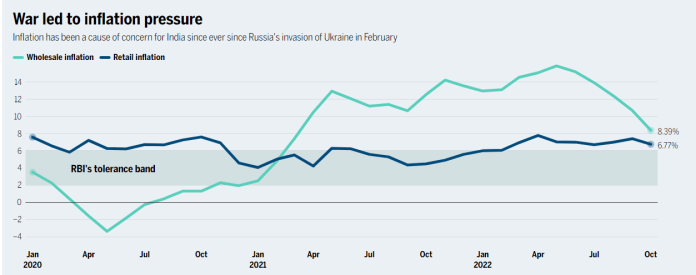

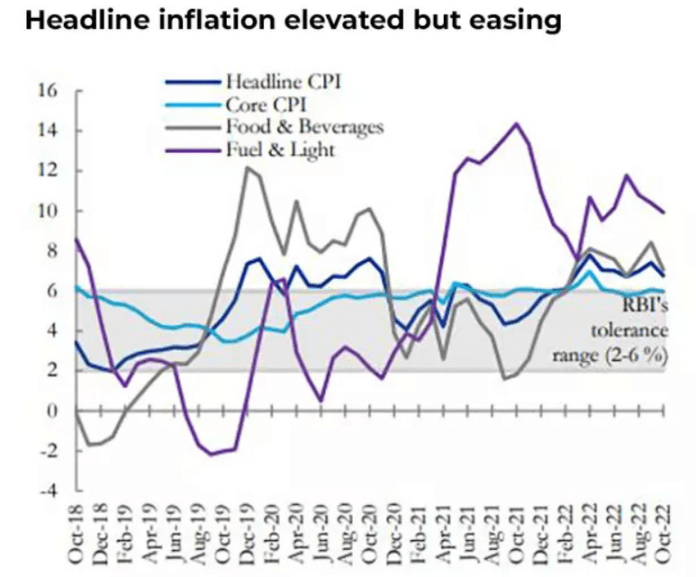

WPI eases, but inflation is a concern

Inflation paced up significantly during February-April 2022 due to higher prices of fuel and food, which constitute about half of the inflation basket, and elevated core inflation. It peaked at 7.8% in April.

Even though the inflation decelerated in October to 6.7%, it is still above RBI’s tolerance band of 2-6%.

Whereas domestic fuel prices have gone down by over 8% since May — after the government cut excise duties — food prices have continued to remain elevated. However, a positive point here is that the prices are on a downward trajectory.

The union government has taken supply-side measures to push down food inflation by easing disruptions in the supply of fertilizers to farmers, export restrictions on wheat and rice products, and reduction in import duties on edible oils.

The Wholesale price index (WPI), which tracks prices at which businesses sell to each other, has been in double digits since April 2021 and averaged 14.2% in the first half of FY23. However, moderating commodity prices and favourable base effects have brought down WPI inflation since June.

Fiscal deficit target on track

The union government is on track to meet its fiscal deficit target of 6.4 %of the GDP for 2022-23 on the back of strong growth in revenue collections, the World Bank said in its report.

High nominal GDP growth in the first quarter supported strong growth in revenue collection, especially Goods and Services Tax (GST), despite tax cuts on fuel.

Despite an increase in spending due to expanded fertilizer subsidies and food subsidies for vulnerable households in response to the commodity price shock, the government is well set to meet its FY22-23 fiscal deficit target of 6.4% of GDP and the general government deficit is projected to decline to 9.6 %from 10.3% in FY21-22 and 13.3% in FY20-21.

Public debt is projected to decline to 84.3 %of GDP in FY23, from a peak of 87.6% in FY21, the report said.

The union government’s revenues increased by 9.5% and spending by 12.2%. As a result, it said, the fiscal deficit touched 37.3% of the annual target in H1 FY22-23, above the 35% of the same half last year.

Reserves

India has one of the largest holdings of international reserves in the world — more than $ 500 billion. While the reserves have declined by about 13% this year, they still provide close to eight months of import cover, based on total imports over the last four quarters (from Q3 FY21-22 to Q2 FY22-23).

As a result, pressure on the Indian rupee has been muted compared to other EMEs.

What others forecast

In October, the International Monetary Fund (IMF) had slashed India’s economic growth forecast to 6.8% for 2022 from 7.4% in its July estimate. However, it sounded a word of caution for major economies of the world and said that global growth is expected to slow further next year as the worst is yet to come.

Fitch Ratings says India could be one of the fastest-growing emerging markets this year and pegs growth at 7%.

Last month, global rating agency Moody’s Investors Service lowered India’s GDP growth forecast to 7% from 7.7% for this year. It expects growth to decelerate to 4. 8% in 2023 and then rise to around 6.4% in 2024.

In a recently released report, Goldman Sachs had said that the Indian economy is likely to lose its growth momentum in 2023 owing to higher borrowing costs and fading benefits from the Covid pandemic reopening. The firm projected India to expand by 5.9% in the calendar year 2023 from 6.9% earlier.

Meanwhile, in its September monetary policy meeting, RBI had lowered its GDP forecast for FY23 to 7% from the earlier 7.2%, citing the impact of geopolitical tensions, tightening global financial conditions and slowing external demand.

{kind=link}

You must log in to post a comment.